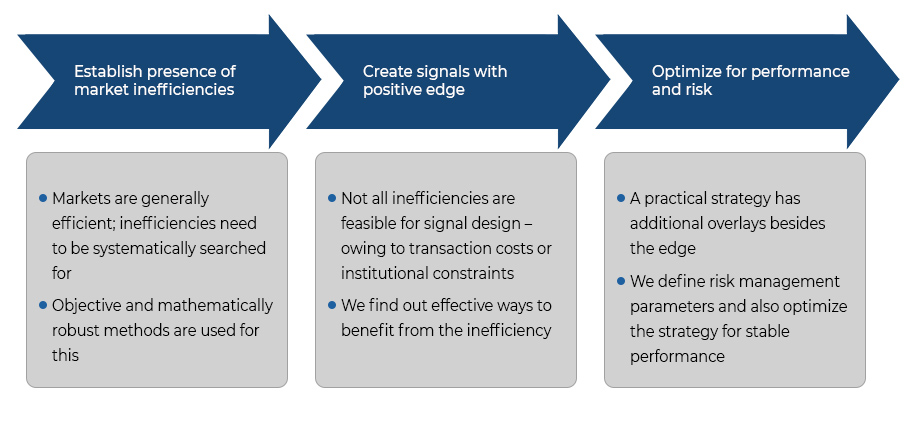

Our belief is that capital markets are ‘broadly’ efficient but have several persistent ‘inefficiencies’ in specific pockets. Hence while it is quite difficult to predict the broad direction of overall market consistently, there are several predictable relationships between characteristics of stocks and their future returns.

However, these relationships are not easy to find. Finding

them requires a combination of disciplined quantitative

analysis, innovations in sourcing and seeing data in novel

ways and a macroeconomic intuition.

At ASQI, this is

what we excel in. We work with not only price-volume data

from the exchange, but also quarterly results published by

companies and several interesting alternate data.

The efficient markets theory of stock prices uses the concept of rational expectations to reach the conclusion that, when properly adjusted for discounting and dividends, stock price changes follow a random walk. According to this line of thinking, the prices of the stocks adjust until the expected returns, adjusted for risk, are equal for all stocks. Equalization of expected returns means that investors’ forecasts become built into or reflected in the prices of stocks. Therefore, the only factors that can change stock prices are random factors that could not be known in advance.

The theory is quite seductive. It has a wide followership and is taught in most business schools and economics departments as gospel truth. The reality is somewhat more nuanced. In the aggregate the capital markets are indeed fairly efficient. Overall market directions are nearly impossible to predict profitably. However, within smaller pockets there are patterns which show meaningful predictability. These patterns on suitable analysis allow one to make market-neutral absolute returns.

This is precisely what we do in our work. Inefficiency in this context is defined as any predictability. The idea is that in a completely efficient capital market, there would be not predictability in securities prices – using either fundamental analysis or quantitative strategies. Hence any predictability is essentially inefficiency.

The inefficiencies need to be spotted carefully though. The most obvious ones are gone quickly. The simplest example is cash-futures arbitrage. The futures which are overpriced, when shorted along with long holding of the same stock, used to deliver returns upwards of 12% per annum in the Indian equity markets through much of 2006-2009. Subsequently as more participants started to exploit this inefficiency, the returns came down. Nowadays, arbitrage generates returns of no more than 6%.

There are other less obvious inefficiencies in the prices of various securities, or in the spreads between their prices. We have developed proprietary techniques to spot and exploit these inefficiencies. These are described in some detail in the page on ‘Research Methodologies’. In a nutshell, finding persistent relationships based on market inefficiencies involves advanced quantitative techniques such as signal processing, machine learning and regression.